Market Activity

Global markets fluctuate amid inflation concerns and upcoming pivotal events

March 3, 2024

Related Links

This fall in the FTSE was disappointing after most of the earnings and data were positive. The Index was dragged down by the remarkable fall of St James’s Place which at one point on Wednesday was down 30% in one single day.

The UK’s largest wealth manager has seen its share price fall 60% over the last 12 months and now sits right at the bottom of the FTSE 100, destined for relegation into the FTSE 250 at the next reshuffle.

The wealth manager has finally been found out and exposed for its outrageously high fees for clients. The whole industry is getting warning shots from the regulator as it iterates that it’s time to put the client, and not the company, first.

There was good news in the form of results from Haleon and Howdens, the latter posted revenues of £2.3 billion. Having grown its market share in 2023 the materials supplier reported ‘encouraging’ revenue trends so far in 2024.

The London Stock Exchange also had a good week and is within weeks of unveiling its first products under a strategic partnership with Microsoft.

The range which has been developed after the US tech giant revealed a 4.2% stake in December 2022, embeds generative AI technologies as the companies look to transform how financial markets participants communicate, research and analyse data.

We are always for progress in the financial markets in the UK as we have fallen behind the US in terms of education and investment in the area.

This week also saw The Nationwide Building Society release data that its house price index rose 0.7% sequentially in February and 1.2% year over year, marking the first annualised increase since January 2023. The Bank of England said mortgage approvals rose to 55,227 — the highest level since October 2022, when the budget plans of former Prime Minister Liz Truss sparked a crisis in the bond market.

In Europe the pan-European STOXX Europe 600 Index ended little changed but remained near record highs. Sticky inflation data prompted investors to reassess the magnitude and timing of interest rate cuts by the European Central Bank in 2024. Major stock indexes were mixed. Germany’s DAX rose 1.81%, while Italy’s FTSE MIB advanced 0.71%. France’s CAC 40 Index lost 0.41%, and the UK’s FTSE 100 Index gave back 0.31%. European government bond yields ended broadly higher.

Both headline and core inflation slowed less than expected in February. Annual consumer price growth in the eurozone slowed marginally to 2.6%. Core inflation decelerated to 3.1%, which was above the consensus estimate of 2.9%.

The European Commission’s economic sentiment indicator also declined unexpectedly to 95.4 in February. European stocks seem to be following the US’s example and ignoring all data. This of course can happen in the financial markets as the real economy separates from the stock market, but it rarely continues without consequence.

In Germany, annual consumer price growth continued to decelerate in February, slowing to 2.7%. However, core inflation and prices of services rose. Private consumption remained weak, with retail sales falling 0.4% sequentially in January, after dropping 0.5% in December. The seasonally adjusted unemployment rate hovered at 5.9% in February — its highest level in more than two years.

Most of the major US benchmarks ended the week higher, with the Nasdaq Composite joining the S&P 500 Index in record territory for the first time in over two years. The month also closed a strong February, with the S&P 500 marking its strongest beginning two months of the year since2019, according to The Wall Street Journal.

The week’s gains were also broad-based, with an equal-weighted version of the S&P 500 Index modestly outperforming its more familiar market capitalisation version. For the year-to-date period, however, the capitalisation-weighted version of the index remained ahead by 409 basis points (4.09 percentage points), reflecting the outperformance of large, technology-oriented growth stocks.

The defining event of the week in terms of market sentiment appeared to be Thursday’s release of the Commerce Department’s core (less food and energy) personal consumption expenditures (PCE) price index.

The index rose 2.8% for the 12 months ended inJanuary, in line with expectations, but the report appeared to calm concerns over the Labor Department’s earlier release of its consumer price index, which showed core prices rising by 3.9%, above expectations of around 3.7%. The core PCE price index is generally considered the Federal Reserve’s preferred gauge of overall inflation pressures.

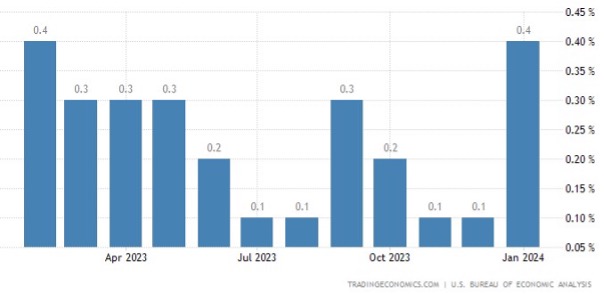

However, as we’ve pointed out so many times, the only reason this number came down, was because the previous January number was even higher. The month-over-month figure released this week was actually a real warning sign.

Below are the monthly figures for the core PCE. January does not look like a move in the right direction at all:

While stocks jumped on the inflation news, it appeared to have a limited impact on the tone of Fed communications. 12 Fed policymakers were scheduled to deliver speeches over the week, and all seemed to see what we saw and echoed the recent narrative that they were in no rush to cut interest rates. Indeed, according to the CME FedWatch Tool, futures markets ended the week pricing in only a slightly higher chance of a rate cut over the next two policy meetings — 24.6% versus 23.4% the week before.

If inflation numbers keep defying expectations (despite what the annual figure shows) the FED is going to have a very difficult time justifying any cuts in the near term at all.

Japanese stocks had another strong week, with the Nikkei 225 gaining around 2.1%, hovering around a new record high and taking February’s gains to about 10.0%. The TOPIX also rose, finishing the week about 1.8% higher.

Stocks in China rose on hopes that Beijing may boost monetary easing measures to stimulate growth. The Shanghai Composite Index gained 0.74%, while the blue chip CSI 300 added 1.38%. In Hong Kong, the benchmark Hang Seng Index gave up 0.82%, according to FactSet.

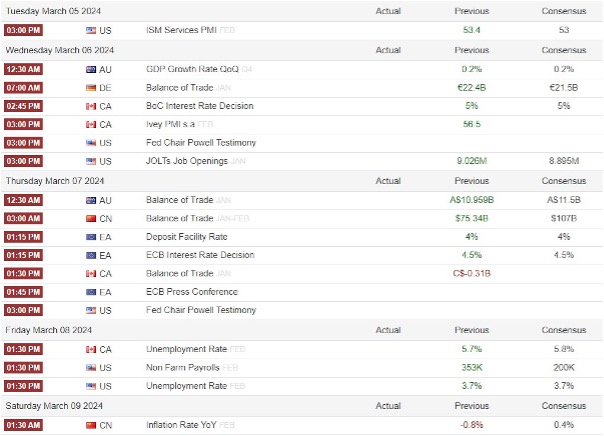

There isn’t anything major out in the UK next week. We will see BRC Retails Sales monitor and the global services PMI on Tuesday as well as the Halifax House Price Index on Wednesday. Nothing to really move the market.

However, the interesting part of the week comes in the form of the Spring Budget on Wednesday. We expect several measures by the Conservative government to bring growth to the UK economy so all eyes and ears will be on that at 12.30pm.

Outside of the UK we have the ECB interest rate decision and press conference on Thursday.

Again, no change is expected from the ECB given the debate has really been about which side of summer their easing will take place. There was a lot of noise among ECB members at the start of the year which may have muddied the ECB’s core message which may need to be fixed at the press conference by Christine Lagarde.

And whilst German inflation figures are softening faster than expected, that is not the case across Europe as a whole which means inflationary pressures persist, which is why we doubt the ECB will signal a dovish pivot over the next couple of meetings.

In the US the primary elections will continue next week, where 16 States vote for their presidential candidates on a day known as “Super Tuesday”. It is almost a given that Biden and Trump will be the nominees for the Democratic and Republican parties, respectively.

Something to watch is whether the Uncommitted campaign convinces enough people to halt support for Biden due to his stance on Gaza, and what proportion of the vote Nikki Haley can maintain in the “closed” primaries next week. Whilst these are not likely to be large market-moving events, they could provide a glimpse of what is to come as the Presidential campaigns kick off later this year.

ISM services PMI will provide a gauge on growth prospects for the US, alongside inflationary pressures via the ‘prices paid’ sub index. Given Fed members continue to push back on imminent rate cuts, employment remains firm and inflation relatively elevated (even if it is softer), data sets such as the ISM can fine-tune expectations of Fed policy.

It is therefore worth noting that the headline index expanded at its fastest pace in five months, employment and new orders also expanded, and prices paid rose shot up to a 12-month high at its fastest monthly pace in nearly three years. If a similar pattern emerges, it points to higher inflationary and growth forces and likely lowers expectations of a June Fed cut.

Next week the Fed Chair has his bi-annual testimony to the House Committee, which is an ideal opportunity for him to (re)shape policy expectations. What traders clearly want to hear is a dovish pivot, but I’m not convinced we’ll get it next week. But it likely means volatility will be hampered in the lead up to his appearance.

Of course, Non Farm Payrolls must at least have a mention; job growth remains strong, unemployment remains low by historical standards and this combination is a key reason as to why the Fed are in no rush whatsoever to announce cuts.

As usual, keep an eye on prior employment reports next week such as Challenger job cuts, initial claims and ADP as it can change sentiment towards Friday's NFP report.

While it is hard to see the markets higher at the end of next week, they continue to find money when the economic climate is looking a little wobbly. Rates tend to curb growth, and rates are, and will remain high, especially in the US, for a lot longer than the markets expect.

If rates fall faster than we expect, it’s because something has broken.

“TPP might just be about to revolutionise investment for the retail market.”

- London Stock Exchange 2020